Why Target Date Funds Dominate The 401(k) Market

A Target Date Fund (TDF) combines a variety of investment strategies into one mutual fund. The concept is that investors, based on their target date of retirement, can simply select one mutual fund that will be managed for them during their entire life. This is because the asset allocation and investments inside the TDF will adjust over time.

A Target Date Fund (TDF) combines a variety of investment strategies into one mutual fund. The concept is that investors, based on their target date of retirement, can simply select one mutual fund that will be managed for them during their entire life. This is because the asset allocation and investments inside the TDF will adjust over time.

The primary factor dictating which investments are inside your TDF will be the number of years until your TDF-year matches the calendar year it is targeting. As a result, the longer the period of time until your expected retirement, the higher your stock allocation will likely be inside the TDF. Keep in mind you are not obligated to select a TDF with the year closest to your expected retirement—but more on that later.

There are other factors that can impact the holdings inside your TDF, including the fund manager’s perception of what is appropriate. For example, I researched a sample of year 2050 TDFs and found a wide range of stock allocation, from a low of about 84% to a high of about 98%. This underscores why it is so important to do your own research.

The good news is you can invest based on characteristics that work for your situation. Start by analyzing the underlying asset allocation for the fund that corresponds to your target year of retirement (or nearest dated fund). For example, if you are 50 and expect to retire at age 67, you would select a fund targeting your retirement year at 17 years from now—a 2035 TDF. However, as we saw earlier, there are differences between TDFs of the same year. So be sure to look for one that you are comfortable with. If no funds in that specific TDF year suit your needs, know that you are not required to invest in the fund that has a year closest to your target retirement year.

Continuing our example of a 50-year-old planning to retire in 2035, if a stock allocation of 78% is too much risk for the investor, then he or she could invest like a 60 year old by selecting a TDF with a closer timeline to retirement (e.g., a 2025 fund which may only have a 55% to 60% stock allocation). Keep in mind that it often makes sense, especially over long periods of time, to invest in stocks. At the same time, it is also important for you to sleep at night, so don’t hesitate to pick your own year and risk level when investing in a TDF.

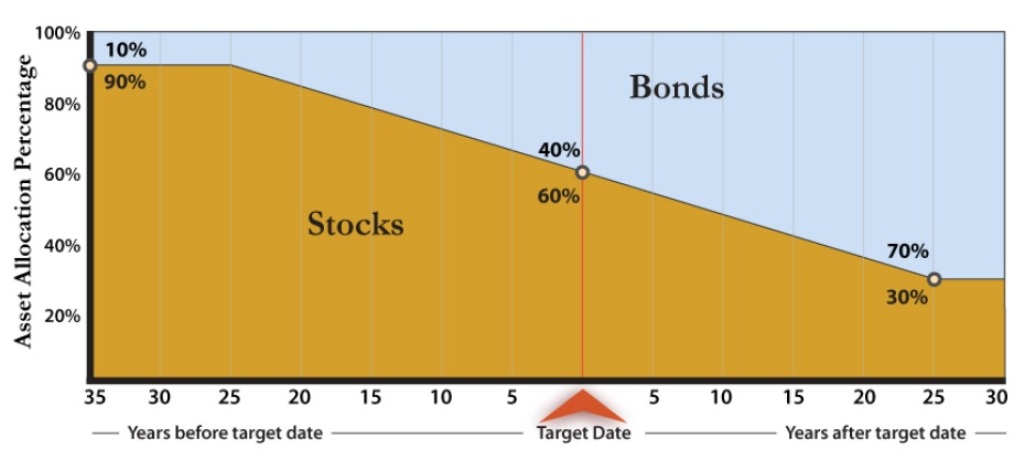

Once you pick your TDF, the manager provides ongoing diversification and risk management. While diversification does not eliminate the risk of loss, it does provide access to different asset classes and styles of investing. This is helpful if you don’t have the time or expertise to handpick your individual investments. Another benefit is that, as you age, the fund will adjust to be more conservative as the target date approaches. This reduction in risk and the internal changes inside the fund is often referred to as the “glidepath” of the fund.

Classically, if you were to invest in a TDF early on in your career, you would be taking on a higher percentage of higher-risk equities while you are further away from retirement, and the manager would subsequently adjust this downward as the fund approaches its target date.

Sample Glidepath of a Target Date Fund Asset Allocation

Sample Glidepath of a Target Date Fund Asset Allocation

Source: www.dol.gov

Target Date Funds are suitable for a wide range of investors, and they are traditionally used in 401(k) plans. As the popularity of these funds grows, more employers are using TDFs as their “Qualified Default Investment Alternative” or “QDIA.” This means that, if a plan participant did not select an investment, the company could direct the participant’s assets into a TDF and not be liable for any potential losses. This employer protection was enacted in the Pension Protection Act of 2006, which helped fuel the popularity of TDFs. According to the Department of Labor, in 2016, 97.6% of retirement plans featured a TDF as the QDIA.

Furthermore, JPMorgan estimates that a whopping 88% of new retirement plan contributions are expected to flow into TDFs by 2019.

Ease of use is perhaps the biggest reason why TDFs have become so popular. Other factors could be their declining costs and the fact that more companies are utilizing low-cost Exchange Traded Funds (ETFs) inside their TDFs.

Target Date Funds are also adding alternative investments, which can be a challenging and risky asset class for investors to select on their own; having that asset class professionally selected and managed by the 401(k) plan sponsor is usually a desirable benefit. Similarly, plan fiduciaries are often happy to include these easy, “do it yourself” TDFs in their 401(k) plan lineup, as doing so can help to manage restrictions and concerns about giving participants individual investment advice.

One drawback may be that TDF managers often select funds solely from one mutual fund family, and that can include historically underperforming funds. Another concern could be that the broad diversification in a TDF may work against an investor if only a few narrow segments of the stock market are driving up the overall market. That said, the risky alternative is for an investor to consistently try to select only top performing managers and the hot areas of the stock market—two things that are virtually impossible to do on a consistent basis and why many investors are migrating to TDFs.

There is no guarantee the TDF will provide adequate income at or through retirement. The principal value of a TDF is not guaranteed at any time, and the values of these funds will fluctuate up to and after the target dates.

Engage us on Facebook

Follow us on Twitter

Tweets by @mymcmedia