Should You Follow These Four Money Rules of Thumb?

Rules of thumb help us make quick decisions without having to consult an expert. But as the definition suggests, it is not reliable for every situation. Below are four financial rules of thumb and when you may or may not want to follow it.

1) Homeownership Rule: Pay at least 20% for down payment.

Ideally, yes, so you don’t have to pay mortgage insurance, which could be a couple of hundred dollars a month.

But a 20 percent down payment can be difficult to save for. If you’d like to buy a $400,000 townhouse in Gaithersburg, we’re talking about an $80,000 down payment. Maybe if you live with your parents and not pay rent for several years, you can save this much.

A 10 percent down payment may be more realistic, given today’s housing prices in the DMV area. What’s more important is you have done your due diligence and determined that buying is better than renting for your situation. Buying is often a better choice if you plan on staying in that place for a long time (say 10 years or more), and your rent is relatively expensive. Best to use a buy vs rent calculator, like the one provided by New York Times or Michael Bluejay.

2) Budgeting Rule: Cap rent or mortgage payment to 25% of gross pay.

Minimizing your rent or mortgage payments can make it easier to achieve other goals like saving for a vacation or retirement. But the right amount will depend on your priorities.

After grad school, I lived with two of my friends, and was paying rent equal to about 16% of my gross pay. This allowed me to pay down my student loans more rapidly, which I was very keen on doing. But there came a point when I just really wanted to live by myself (I’m an introvert), and swallowed paying 28 percent of my salary to housing. It was higher than what I wanted, but I felt it was the right time to transition. Eventually this ratio went down to a more acceptable level as my salary increased.

If you’re a young parent who is willing to pay a premium to be near good schools, it may make sense to pay that extra $200 each month.

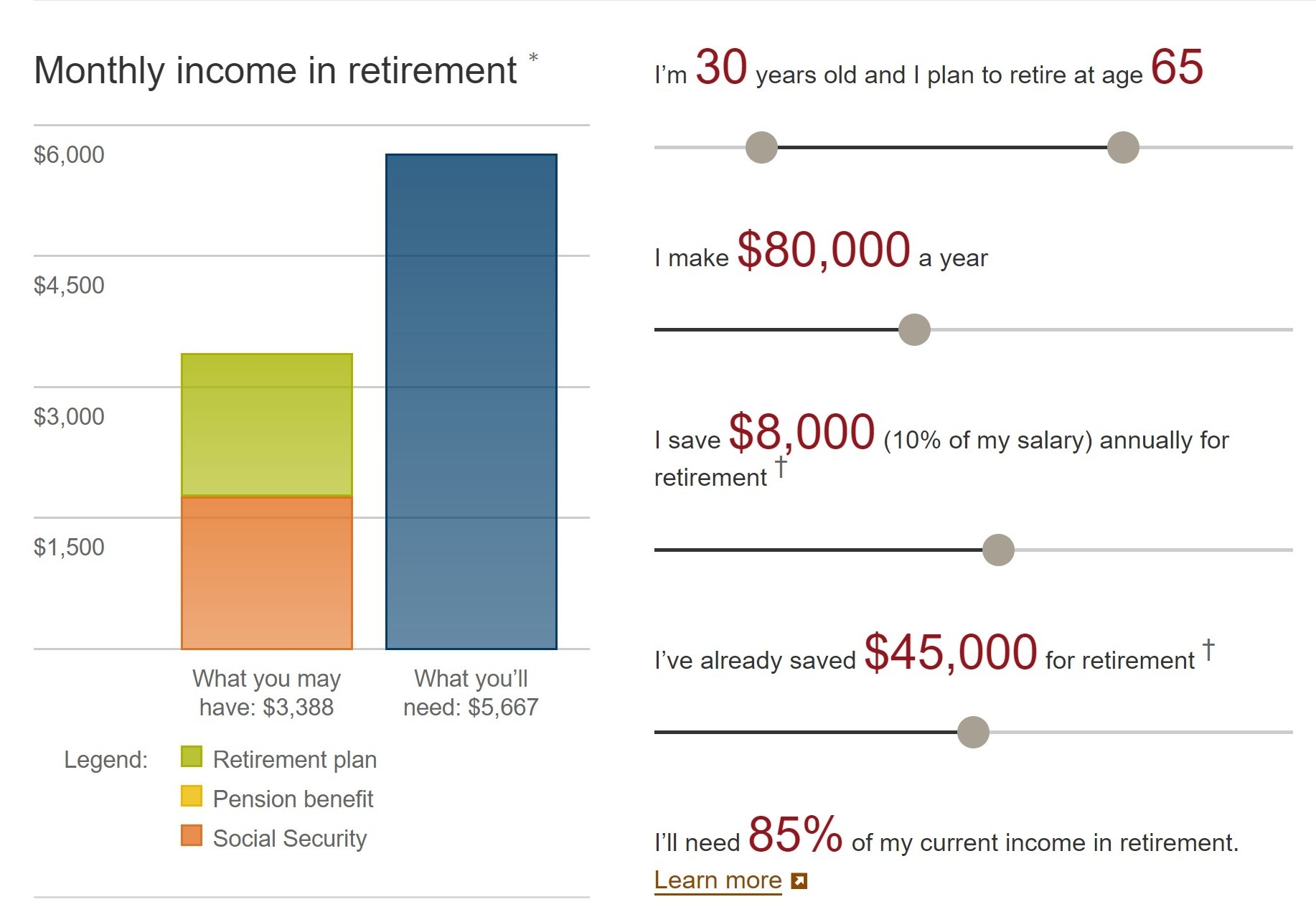

3) Retirement Rule: Save 10% of gross income towards retirement.

I’m currently doing pro-bono work for Catholic Charities’ Financial Stability Network. I coach a 65 year-old non-profit professional on his finances. It broke my heart to see that he only has $28,000 in retirement savings. I had to explain to him that he would need to work longer than he expected to. This type of encounter inspires me to continue urging young professionals to save as much as possible.

Saving 10 percent is better than saving three percent. But even then, this may only be sufficient if you just graduated from college, or receive a strong 401(k) match from your employer.

Most of us need to be saving at least 15 percent of our gross income towards retirement. Likely because we started saving late, and the realistic return for an aggressive investment portfolio is significantly lower today (more on this below).

Retirement income calculator of Vanguard

If your employer matches your contributions up to five percent of your salary, that’s a huge help. I’ve seen a few that match up to 10 percent! Factor employer 401(k) matching when you’re considering a job offer.

To know what you personally need to be saving, it’s best to use a retirement calculator, where you can plug in your numbers, and it will give you an indication on how much you need to be saving.

Just be careful about the assumptions. For example, if you put an unrealistic rate of return, the results will be overly optimistic.

4) Investing Rule: A diversified portfolio of U.S. stocks will return an average of 10% per year.

It is true that U.S. stocks, as represented by the S&P 500, has historically had an average annual return of about 10 percent (9.53 percent to be exact, the geometric average between 1928 to 2016).

But it is not prudent to assume that this strong performance will continue. As we know from Kung Fu Panda, the past is history, tomorrow is a mystery.

If you do the math today, U.S. stocks’ expected annual return is closer to three percent: two percent from dividend yield, 3.3 percent from economic growth, less 2.7 percent from being overvalued.

At District Capital, we urge our clients to have a more diversified portfolio that includes other asset classes to improve expected long-term returns and risk profile.

Engage us on Facebook

Follow us on Twitter

Tweets by @mymcmedia